Hello, World!

I’m Noah Dett, and I’m honored to welcome you to the Choose Credit blog. “Come Fly With Me…”

I’ve been inspired to begin this conversation with you after reading countless reports of increasing fears of credit within my generation (spoiler alert: I’m a twenty-something Millennial). Here are a few recent headlines:

“Visa Jumps on Debit Spending by Credit-Averse Millennials” (Bloomberg – Apr. 25, 2018).

“Why Millennials Are Ditching Credit Cards” (Fortune – Feb 27, 2018).

“Millennials Spend More on Debit Purchases Than Credit” (U.S. News & World Report–Apr 26, 2018).

I won’t get into too much detail about the causes of these fears of credit, but such fears could be a result of:

- the aftermath of the Great Recession and much of Generation X’s spending habits;

- a lack of credit, debt, and/or financial education;

- enough debt already (STUDENT LOAN DEBT!!! Sorry, I have a “friend” who may be dealing with this at the moment. I digress…).

All of this brings us to the original question: credit or debit?

Debit seems easy and convenient enough, right? Your debit card is the free version of previous generations’ checks, and it’s easier to use. It’s directly linked to your checking account. It enables you to instantly convert checking account funds into cash at the ATM. It’s less likely to be subject to card processing fees. Plus, you know that just like checks, you should treat your debit card like cash from your checking account.

So what about credit? Credit’s associated with debt, right? Shouldn’t debt be avoided at all costs?

Short answer: In most cases, credit beats debit.

DISCLAIMER: I am NOT saying credit is always better than debit; this depends on your financial situation and the costs/benefits associated with specific credit and debit accounts.

Long[er] answer: Credit beats debit in most cases due to the prospects of:

(1) financial rewards—Earn Points and Stretch Your Dollar—for purchases you’re already making.

(2) flexibility – making the exact same amount of payment(s) on your credit card that you’re already making with your debit card, except your payment(s) isn’t due for weeks later (minor lesson from Finance 101: due to inflation and other factors, paying the exact same amount later maximizes value for you; it costs you less to give me a dollar two weeks from now than if you had to give it to me today).

(3) security – two kinds: financial emergency security (where an unexpected event occurs that causes an imminent need for money that cannot be fully paid from a checking account) and security from fraud (hackers and criminals aiming to steal your money and/or personal information). While some debit cards offer protection in these areas, credit cards are still your best bet. Plus, just think about it: would you rather have someone hack your credit card information (which is easily changeable and designed for fraud protection) or a direct link to your bank account?

(4) perks – I’ll save the details of this benefit for later posts, but how does elite hotel status, GlobalEntry/TSA Pre-Check for free, Uber/Lyft credits, airline travel credits, resort credits, etc. sound?

(5) Other reasons to be discussed in later posts… Stay tuned.

My goals for this blog are simple:

- Improve Your Score.

- Earn Points.

- Stretch Your Dollar.

These goals and various tactics for how to accomplish them will be the subject of upcoming Choose Credit posts, but for now, let’s keep it simple and have a word about credit. Unless you’ve been living under a rock, my guess is you know a thing or two about credit and credit scores. But let’s review…

Credit

Experian, one of the U.S.’s “Big Three” credit bureaus, defines “credit” as “borrowed money that you can use to purchase goods and services when you need them.” Credit can be:

1) Revolving credit – think traditional credit card; you are given a “line of credit,” or a preset amount of money from a bank or financial institution that you are allowed to borrow up to the maximum credit limit. You carry a balance (the revolving debt) each month and make payments to reduce/eliminate that balance (note: ALWAYS aim to pay off your balance IN FULL each month to avoid interest charges; there are situations where this may not be possible, but as I’ll talk about later, pay off in full is a MUST to meet the goals of this blog.).

2) Charge cards – similar to credit cards, but this type of card requires that you pay the total balance in full each month.

3) Service credit – think of your agreements with service providers (electric service, phone service, internet service, etc.). These agreements generally require monthly payment for the applicable service.

4) Installment credit – think car loans and mortgages. The lender/creditor loans you a certain amount of money and you agree to repay that money and associated interest in regular installments of a fixed amount over a designated period of time.

Having good credit is critically important if you want to make a major purchase, open a new account, start a business, get hired for a new job, rent a new place—the list goes on…

So how do businesses and people determine whether you are worthy enough for them to grant you a loan, approve you for a credit card, or start a new relationship with you (i.e. your creditworthiness)?… They’ll consider a variety of factors—including your income— but the universal measure of creditworthiness is your credit score.

Credit Score

Your credit score is a three-digit number that indicates how financially trustworthy you are. Think of it like grades in school (A, B, C, D, F); except in this case, the higher the number the better (e.g., a score of 800 is better than 750).

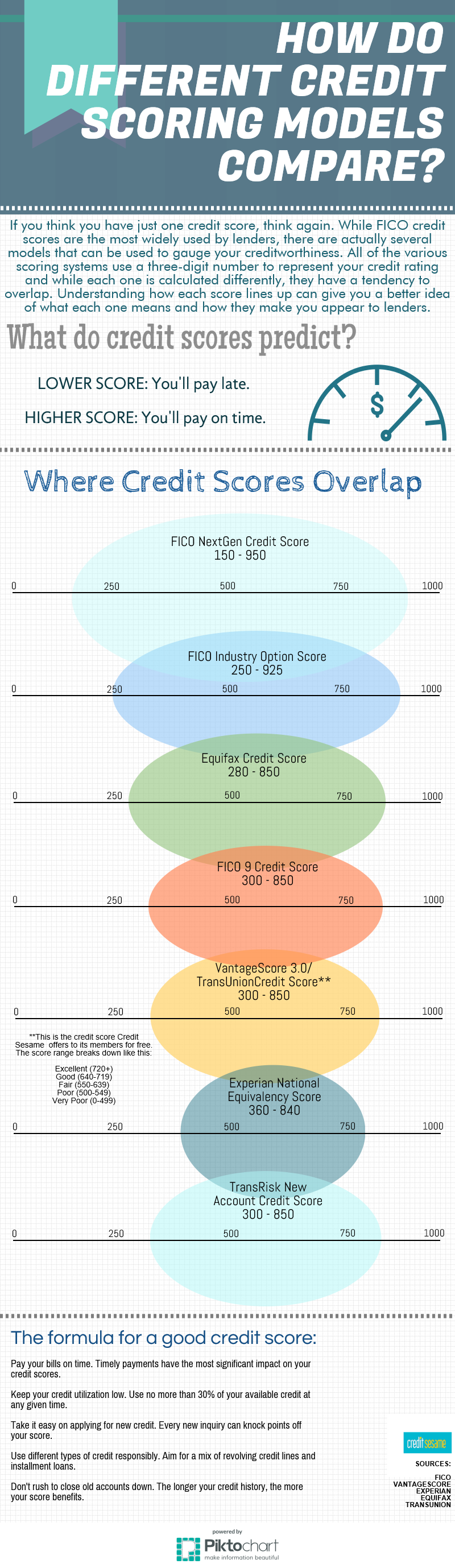

As I said before, there are three major credit bureaus (Experian, Equifax, and TransUnion; the “Big Three”). Each of the Big Three have their own credit score methodologies and ranges. Some of the Big Three even have different credit scores within the same bureau.

You’ve likely also heard of the term “FICO score.” FICO refers to the Fair Isaac Corporation, which created credit risk scoring in 1960. A FICO score is another type of credit score that is often utilized by U.S. lenders.

Take a look at the different credit score models and ranges in the graphic below, courtesy of our friends at Credit Sesame.

So what do YOU think?

- Could it really be that credit is better than debit?

- Are you interested to learn more?

- Am I, Noah Dett, crazy for starting this conversation?

I’m of the opinion that all of us are crazy in our own way.

My hope is that Choose Credit blog can be a collaborative forum for learning and discussion of the tremendous offerings available in the world of credit. If you haven’t learned anything new from this post, stick around for the next one and the one after that and the one after… Also, please post comments, questions, and suggestions that you have, and share this with your family and friends. The more the merrier!

I look forward to embarking on this Choose Credit journey with all of you!

“People never grow up, they just learn how to act in public.”—Bryan White

Great information. Very well written and easy to follow. Looking forward to follow up posts

LikeLike

Wow!

LikeLike

Hey Joey ggggggG-Unit! This was very informative. I’m on the edge of my seat awaiting the next post.

LikeLike

This is well-written sir. I support the notion that millennials fear using credit cards because they don’t understand the basics of debt. They assume that all debt is bad and that carrying any debt is unacceptable. The impact of the Gen Y is already changing e-commerce, technology, and global communication. Goldman Sachs expects that the spending power of the largest generation will soon exceed that of the Baby Boomers. Many of the apps and financial instruments are today being designed for this generation to improve their savings rate, engage the stock market, and recognize the value of effective debt management. As the millennials will soon have USD 60+ Trillion in assets, the SEC and other government agencies are trying to figure out how to better interface with this group of powerful investors who pride themselves on banking and investing differently from their parents’ generation. Credit cards are no exception-they need to cater to the millennial generation and innovate/compete on the basis of a markedly enhanced reward platform that matches value to the Gen Y buying power.

LikeLike